Before you even think about writing an advert or setting a rent price, you need to make one fundamental decision: are you renting out a spare room in your own home, or are you letting a completely separate property?

This single choice sets the entire stage. It determines your legal responsibilities, how much tax you'll pay, and what your day-to-day life as a landlord will look like. Getting this right from the start is absolutely crucial.

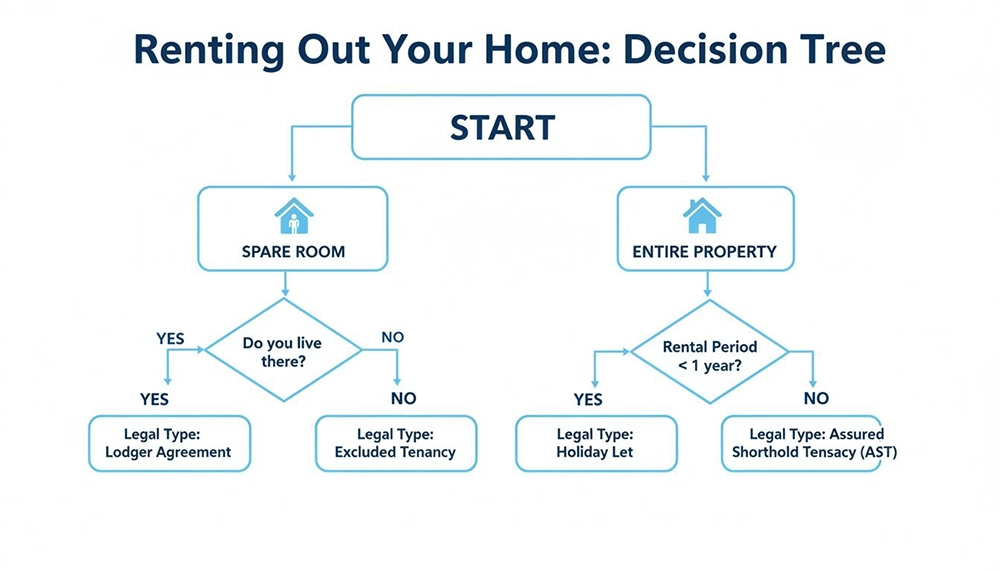

Your First Move: Renting a Room vs. an Entire Property

The path you take dictates the entire legal framework you'll be working within. This isn't just about sharing a kitchen; it's about two entirely different legal agreements, each with its own set of rules, responsibilities, and benefits. It's a big decision, so it's well worth exploring the pros and cons of renting out your house before you commit.

This decision tree gives a great visual overview of the different routes you can take.

As you can see, that initial choice branches out into very distinct legal paths and landlord duties.

The Lodger: A Simpler Starting Point

Got a spare room? Taking on a lodger is often the easiest and most accessible way to start earning some rental income. A lodger is someone who lives in your main home and shares common areas with you, like the living room or kitchen.

This setup is governed by a 'licence to occupy', which is much more flexible than a formal tenancy agreement.

The big advantages of going down this route are:

- A much easier eviction process. If things don't work out, you only need to give your lodger 'reasonable notice'—usually the same length as their rental period, like one month. You don't need a court order.

- The Rent a Room Scheme. This is a fantastic government incentive that lets you earn up to £7,500 a year completely tax-free from a furnished room in your main home. This perk isn't available if you're letting a whole property.

The key takeaway here is the reduced legal headache. Because you're living in the property, you have more control, and the law recognises the personal nature of the arrangement by giving you more flexibility. It's an ideal first step for many homeowners.

The Tenant: A Formal Landlord-Tenant Relationship

If you're letting a separate property—maybe a house you've moved out of or a buy-to-let investment—you're stepping into the shoes of a traditional landlord. The person living there is a tenant, and their rights are protected by an Assured Shorthold Tenancy (AST) agreement.

This is a more formal arrangement with stricter responsibilities:

- Deposit Protection. You are legally required to put the tenant's deposit into a government-approved scheme within 30 days of receiving it.

- Stricter Eviction Rules. To get your property back, you have to follow a precise legal process involving Section 21 or Section 8 notices, which can be a lengthy affair.

- Full Tax Liability. Every penny of rental income is taxable after you've deducted your allowable expenses. The Rent a Room scheme doesn't apply here.

What About Houses in Multiple Occupation (HMOs)?

Planning to let a larger property to several people who aren't a family? You could be running a House in Multiple Occupation (HMO), which brings another layer of regulation.

Generally, a property becomes an HMO if at least three tenants live there, forming more than one household, and they share a toilet, bathroom, or kitchen. In England and Wales, you'll need a mandatory HMO licence if the property has five or more occupants.

On top of that, local councils can bring in their own 'additional licensing' schemes, so you must check their specific rules. Getting caught running a licensable HMO without a licence can result in massive penalties, including unlimited fines.

Whether you're looking to fill a single room or manage a larger house share, a great place to start is to register as a landlord on Rooms For Let and begin connecting with people looking for a place.

Getting Your Property Tenant-Ready

So, you’ve decided on your letting strategy. Now comes the crucial part: transforming your space from a simple property into a safe, legal, and genuinely appealing home for someone. This is about so much more than just a quick tidy-up and a lick of paint.

Getting this stage right is your first real test as a landlord. It’s where you lay the groundwork to attract the best tenants, prevent those dreaded late-night calls about a leaky tap, and steer clear of serious legal trouble. Think of it as setting the stage for a smooth, professional, and profitable letting experience.

Your Legal Safety Obligations

Before a tenant even thinks about moving in, you have a legal duty to make sure the property is safe. This isn't just good practice; it's the law, and failing to comply can land you with eye-watering fines or worse. The big three you need to have sorted are gas, electrical, and fire safety.

Think of these certificates as your property's MOT. They are non-negotiable and prove you’ve done your bit to keep your tenants safe.

Gas Safety Record (CP12): This is proof that a Gas Safe registered engineer has thoroughly checked every gas appliance, flue, and bit of pipework. It’s a legal requirement to get this done every 12 months and you absolutely must give a copy to your tenants.

Electrical Installation Condition Report (EICR): An EICR is a deep dive into your property's wiring and electrical systems, confirming they’re safe and up to standard. A qualified electrician needs to carry this out at least every five years.

Fire Safety Measures: The rules are clear. You must have at least one working smoke alarm on every floor of the property that’s used as living space. On top of that, a carbon monoxide alarm is mandatory in any room with a solid fuel-burning appliance, like a wood-burning stove or an open fire.

Remember, these are the bare minimums. If your property is classed as an HMO (House in Multiple Occupation), your obligations will be stricter. Always double-check the specific requirements with your local council to stay on the right side of the law.

To help you keep track, here’s a quick summary of the essential checks.

Landlord Safety Certificate Checklist

This table breaks down the mandatory safety certificates you'll need before you can let your property in the UK.

| Requirement | What It Covers | Frequency |

|---|---|---|

| Gas Safety Record (CP12) | Checks all gas appliances, flues, and pipework are safe. | Annually (every 12 months) |

| EICR | Assesses the safety of the property's electrical installations. | At least every 5 years |

| Smoke Alarms | Functioning smoke alarms must be installed on every storey. | Tested at the start of each tenancy |

| Carbon Monoxide Alarms | Required in any room with a solid fuel appliance. | Tested at the start of each tenancy |

Having these documents in order isn't just about compliance; it shows tenants you're a responsible landlord who takes their safety seriously.

Smart Repairs and Pre-Tenancy Checks

Once the major legal safety checks are sorted, it’s time to put on your inspector’s hat and look at the property’s general condition. A small drip or a sticking window might seem minor to you, but they can quickly escalate into bigger problems—and bigger bills—once someone is living there.

Walk through the property as if you were viewing it for the first time. Be critical. Look for those little things that drive tenants mad: dripping taps, mould in the bathroom sealant, or draughty windows. These are not only off-putting but can lead to disputes down the line. A thorough pre-tenancy inspection is vital; learn how to check for bed bugs and other pests to avoid nasty surprises later on.

Focus your energy on these areas for the biggest impact:

- Plumbing: Check for any leaks under sinks and make sure the toilets flush properly. Good, consistent water pressure is a massive selling point.

- Windows and Doors: Ensure every lock works smoothly and that windows open, close, and lock securely. This is a basic security must-have.

- Décor: You can’t go wrong with a neutral colour scheme. Touch up any scuffs on the walls and consider replacing worn-out carpets. It makes the whole place feel fresh, clean, and ready for a new occupant.

- Exterior and Garden: Don’t forget the outside! A tidy garden, a clean front door, and a clear path create a fantastic first impression before they even step inside.

Furnished or Unfurnished: The Strategic Choice

One of the biggest calls you’ll make is whether to offer the property furnished or unfurnished. There’s no single right answer here—it all comes down to your property, its location, and the type of tenant you’re hoping to attract.

For instance, a city-centre flat aimed at students or young professionals will almost certainly get more traction if it’s furnished. These tenants are often moving from city to city and don’t want the hassle or expense of buying and moving their own furniture. On the flip side, a three-bedroom house in a quiet suburb will likely appeal to a family who already has their own belongings and is looking to settle in for the long term.

Here’s a quick breakdown to help you weigh it up:

| Feature | Furnished | Unfurnished |

|---|---|---|

| Target Tenant | Students, young professionals, short-term lets | Families, long-term renters |

| Potential Rent | Can often command a slightly higher rent | Generally a little lower |

| Landlord Costs | Significant initial outlay for furniture, plus ongoing replacement costs | Minimal initial costs |

| Management | More wear and tear to manage; a highly detailed inventory is essential | Less to worry about day-to-day; simpler inventory |

If you go down the furnished route, just remember this critical rule: any upholstered furniture you provide (sofas, armchairs, mattresses) must meet the latest fire safety standards and have the correct labels to prove it. This is another one of those non-negotiable legal duties you can’t afford to miss when renting out your home.

Getting Your Price and Advert Right

So, your property is safe, compliant, and looking the business. Now for the crucial part: setting the right rent and getting the word out. This is a bit of a balancing act. Aim too high, and you’re looking at costly empty periods that bleed profits. Price it too low, and you're leaving cash on the table every month.

The trick is to get inside the head of a potential tenant. What are they searching for? Where are they looking? And what’s the going rate for a place like yours, right here, right now? Nailing this is the foundation of a successful let.

How to Set a Competitive Rent

Guesswork is your enemy here. Your rental price has to be rooted in solid, local market data. A property’s rental value isn’t what you hope to get; it’s what similar properties nearby are actually renting for.

It's time to become a local expert. Pour a coffee and spend an hour browsing the big portals like Rightmove and Zoopla, as well as specialist sites like Rooms For Let. Hunt for properties that are a close match to yours in size, condition, and location.

Keep a sharp eye on these details:

- Property Type: If you have a two-bed flat, you should only be comparing it with other two-bed flats. Simple.

- Location: Don't underestimate the power of a few streets. Being closer to a station or a good school can make a real difference to the price.

- Condition: This is where you need to be brutally honest. How does your decor and finish really stack up against the competition?

- Furnishings: Make a note of whether comparable lets are furnished or unfurnished and factor that into your own pricing.

Here’s a pro tip: focus on properties marked as 'Let Agreed'. This shows you the price the market was willing to pay, which is far more useful than an ambitious asking price on a property that’s been sitting empty for weeks.

Understanding Current UK Rental Market Trends

It also pays to understand the bigger picture. The UK rental market is always on the move, with supply and demand constantly nudging prices up or down.

For instance, at the start of 2025, the average rent outside London reached a record £1,349 per month, but the frantic pace of growth has cooled off. An 18% year-on-year increase in the number of available rental homes is giving tenants more choice, which means landlords have to price their properties competitively to get noticed.

While tenant demand is still strong—averaging 12 enquiries for every available property—it has softened slightly. This just reinforces the need for a realistic pricing strategy. A bit of research into current UK rental market trends will give you the context you need to make a smart decision.

Crafting an Advert That Demands Attention

Once you've landed on a competitive price, your next job is to create an advert that stops scrollers in their tracks. Think of your listing as your shop window – it has to be compelling.

High-Quality Photos Are Non-Negotiable

This is, without a doubt, the most important part of your advert. Poor, dark, or blurry photos will get your listing skipped over, no matter how lovely the property actually is.

- Tidy and Declutter: Before you even think about a camera, do a deep clean and hide all your personal bits and bobs.

- Let There Be Light: Open every curtain and blind. Shoot during the day. Bright, airy photos are universally appealing.

- Show Off the Best Bits: Use wide shots to make rooms feel spacious and focus on key selling points like that modern kitchen or the garden.

- Lead With Your Best Shot: Your main image should be of the most impressive space, which is usually the living room or kitchen.

Write a Description That Sells a Lifestyle

Don't just list facts; sell the dream. Instead of "Two bedrooms," try something like, "Two spacious double bedrooms, perfect for professional sharers or a young couple."

Your description needs to be easy to scan, highlighting the key info tenants are looking for. Start with a punchy introduction, use bullet points for the main features, and finish by painting a picture of the local area. Mention the nearby park, that great pub on the corner, or the 10-minute walk to the station. Help them imagine their life there.

Putting together a great ad is simple on platforms built for landlords. You can check out the different Rooms For Let advert prices and features to see how easily you can get your property in front of thousands of active room-seekers, often with a free option to get you going.

Getting the Paperwork Right: Your Legal and Financial Duties

Once you’ve found your ideal tenant and they’re ready to move in, you officially switch hats from property owner to landlord. This isn’t just a change in title; it comes with a handful of critical legal and financial responsibilities that you simply can’t afford to get wrong.

Getting these fundamentals sorted from day one is the bedrock of a successful tenancy. It protects you, your tenant, and your investment, making sure everything is above board.

Think of these duties not as boring admin, but as the legal framework of your entire rental agreement. Slip up here, and you could be facing hefty fines, messy legal battles, or even find yourself unable to regain possession of your property down the line.

Conducting Right to Rent Checks

Before anyone moves in, you have a legal duty to check that every prospective tenant aged 18 and over has the right to rent property in the UK. This applies to everyone who will be living there, even if their name isn't on the tenancy agreement itself.

You’ll need to check their original documents in person or, for those with a 'share code', use the Home Office's online checking service. The aim is simple: to confirm they have a legal right to live in the UK for the tenancy period.

Acceptable documents often include:

- A UK or Irish passport

- A valid visa or biometric residence permit

- Official documents proving a right of abode in the UK

It’s absolutely vital that you take copies of these documents, note down the date you did the check, and keep them somewhere safe for the entire tenancy, plus one year after it ends.

Protecting Your Tenant's Deposit

If you’re taking a deposit for an Assured Shorthold Tenancy (AST) in England and Wales, the clock starts ticking the moment you receive it. You are legally required to protect that money in a government-approved tenancy deposit scheme (TDP) within 30 days.

The three approved schemes are:

- Deposit Protection Service (DPS)

- MyDeposits

- Tenancy Deposit Scheme (TDS)

But just protecting the cash isn't enough. You must also give the tenant the official paperwork from the scheme, known as 'prescribed information'. This tells them exactly where their money is and how the scheme works. Failing on either count can lead to a penalty of up to three times the deposit amount.

This is hands-down one of the most common and expensive mistakes new landlords make. It’s a straightforward task, but the penalties are severe. Always, always get proof that you've served the prescribed information. An email with a read receipt is a good start.

Securing the Right Landlord Insurance

Heads up: your standard home insurance policy is null and void the moment a tenant moves in. It’s designed for owner-occupiers, not for the unique risks that come with renting out a property. You need a specialist landlord insurance policy.

This kind of insurance is built to cover rental-specific scenarios, such as:

- Loss of rent: Crucial if your property becomes unliveable after something like a fire or flood.

- Property owner's liability: This protects you if a tenant or visitor gets injured at your property and decides to make a claim.

- Malicious damage by tenants: Not always standard, but often a very worthwhile add-on for peace of mind.

Don't just assume your current policy will do. Call your insurer, tell them your plans, and switch to a proper landlord policy. It's the only way to be fully protected.

Understanding Your Tax Obligations

Any money you make from rent is taxable income, and you need to declare every penny of it to HMRC. With the private rented sector making up a stable 20% of households in the UK, it’s an area the tax authorities keep a close eye on.

You'll need to file a Self-Assessment tax return each year. How much tax you pay depends on your total income from all sources and which tax band you fall into.

The good news? You can deduct certain allowable expenses from your rental income to lower your tax bill. These are costs that are 'wholly and exclusively' for the purpose of renting out the property.

Common allowable expenses include:

- Letting agent and management fees

- Landlord insurance premiums

- Maintenance and repair costs (note: this doesn't include property improvements)

- Accountancy and legal fees

- Direct costs you cover, like council tax or utility bills

Keeping meticulous records is non-negotiable. Seriously, track every penny. A great tip is to open a separate bank account just for your rental business—it makes managing income and expenses infinitely easier at tax time. For more in-depth guidance, have a look through the landlord guides on the Rooms for Let blog.

Finding and Managing the Right Tenants

Once your property is ready and the advert is live, you’re stepping into what is arguably the most critical part of the whole process: choosing who gets to live there. The success of your entire venture really hangs on this decision. Get it right, and you'll have a great tenant who pays on time and looks after the place. Get it wrong, and you could be facing endless stress and financial headaches.

This isn't about being judgemental; it's about running a professional screening process to protect your investment. From hosting effective viewings to carrying out meticulous checks, every step is designed to give you peace of mind that you're making a sound choice.

Conducting Productive Viewings

Your advert has done its job, and the enquiries are rolling in. It's time to show people around. The best way to think of a viewing is as a two-way interview. You're sussing them out, and they're deciding if your property feels like home.

To get the most out of every viewing:

- Stick to individual appointments. Group or 'open house' viewings feel chaotic and rushed. They stop you from having a proper chat with anyone, which is the whole point.

- Have your answers ready. People will inevitably ask about council tax bands, what the average utility bills are, and what the local area is like. Knowing this stuff off the top of your head shows you're an organised, professional landlord.

- Ask open-ended questions. Instead of a closed question like "Do you have pets?", try something more conversational like "So, can you tell me a bit about who'll be living here?" It encourages people to open up and gives you a much better feel for them.

The Power of Thorough Referencing

When you've got a promising applicant, it’s time to do your homework with proper tenant referencing. This is where you verify everything they’ve told you and get an objective picture of their reliability. It's tempting to skip this, especially if you get a good vibe from someone, but you absolutely must not.

A comprehensive referencing check should always cover:

- A credit check. This uncovers their financial history, flags any County Court Judgements (CCJs), and helps confirm they are who they say they are.

- An employer's reference. You need this to confirm their job, salary, and how stable their income is. A solid rule of thumb is that a tenant's gross annual income should be at least 30 times the monthly rent.

- A reference from their previous landlord. This is gold dust. Ask specific questions: Did they always pay rent on time? How did they leave the property? Crucially, would you rent to them again?

Relying on a gut feeling is one of the biggest mistakes a new landlord can make. Professional referencing provides the hard evidence you need to back up your instincts and ensure you are renting out your home to someone reliable.

Securing the Right Agreement

With your ideal tenant lined up, the next step is to make it official with a legally sound contract. The type of agreement you need depends entirely on whether you'll be living in the property too.

- Lodger Agreement: If you’re a live-in landlord renting out a room, you'll use a lodger agreement (sometimes called a 'licence to occupy'). This is a less formal contract that gives you more flexibility, especially when it comes to ending the arrangement.

- Assured Shorthold Tenancy (AST): This is the standard contract in England and Wales for renting out a whole, separate property. An AST provides tenants with specific legal protections and clearly spells out the rights and responsibilities for both of you.

Whichever you use, make sure it clearly states the rent amount, the payment date, the length of the tenancy, and any specific house rules on things like pets or smoking.

Why an Inventory Report is Non-Negotiable

Before you even think about handing over the keys, there’s one last piece of admin that is absolutely essential: a detailed inventory report. This document is a snapshot of the property's condition and all its contents right at the start of the tenancy, backed up with time-stamped photos.

This report is your single best defence against deposit disputes down the line. Without a clear 'before' picture, it's your word against theirs, and proving that any damage happened during their tenancy is almost impossible. Be meticulous. Note every scuff on the skirting boards and every light scratch on the worktops. Once it's done, both you and the tenant should sign it to confirm you agree on the property’s condition from day one. A bit of diligence now can save you a fortune and a world of hassle later.

The UK rental market remains strong, with some forecasts suggesting a cumulative rent increase of nearly 18% by 2029. We're seeing powerful growth in regions like the North East, with a 9.7% annual rise, highlighting the financial potential for landlords. This also underlines just how important it is to secure reliable tenants to protect that income stream. You can learn more about these market trends by exploring the latest research on UK rental price growth.

Common Questions About Renting Out Your Home

Stepping into the world of renting out your home can feel like learning a new language. It’s packed with unfamiliar terms and regulations, so it’s completely natural to have questions.

Here, we’ll tackle some of the most common queries we hear from new and even experienced landlords, giving you clear, straightforward answers to help you move forward with confidence.

Do I Need to Tell My Mortgage Lender?

Yes, absolutely. This is non-negotiable. Your residential mortgage agreement almost certainly requires you to inform your lender before you let out your property. Keeping them in the dark isn't just a minor oversight—it could be considered mortgage fraud, which has severe consequences.

Your lender might grant you a 'consent to let', which is temporary permission to rent out your home on your current mortgage. This might involve a one-off fee or a slight increase in your interest rate. Alternatively, they may require you to switch to a proper buy-to-let mortgage, which is specifically designed for rental properties.

Failing to inform your lender is a huge gamble. In a worst-case scenario, they could demand you repay the entire mortgage loan immediately. It’s a simple conversation that protects you from a world of trouble.

What Is the Difference Between a Lodger and a Tenant?

The main difference comes down to one simple question: do you, the landlord, live in the property as your main home?

A lodger rents a room in your home and usually shares common areas like the kitchen or living room with you. They have a 'licence to occupy', which offers them fewer legal protections and makes it much simpler for you to end the arrangement.

A tenant rents a whole, self-contained property and has exclusive access to that space. Their rights are protected by a formal contract, typically an Assured Shorthold Tenancy (AST), which governs everything from deposit protection to the eviction process.

This distinction fundamentally changes your legal obligations. Ending an agreement with a lodger generally just requires 'reasonable notice', whereas removing a tenant involves following a strict and formal legal process.

How Much Tax Will I Pay on Rental Income?

Any money you earn from renting out your property is taxable income. You’ll need to declare it to HMRC through a Self-Assessment tax return. This rental profit gets added to your other earnings (like a salary from a job), and you pay Income Tax on the total based on your personal tax band.

The good news is you can lower your tax bill by deducting 'allowable expenses'. These are costs you’ve incurred purely for the purpose of renting out the property. Common examples include:

- Letting agent fees

- Landlord insurance policies

- Costs for maintenance and repairs (but not improvements)

- Accountancy fees for your tax return

If you’re just taking on a lodger in your own home, you might be able to use the government's Rent a Room scheme. This brilliant scheme allows you to earn up to £7,500 per year completely tax-free. It’s a major perk for live-in landlords but doesn’t apply if you're letting out a separate property.

Whatever you do, keep meticulous records of every penny coming in and going out. It will make your tax return a breeze and ensure you claim every single deduction you're entitled to.

Ready to find the perfect person for your spare room? Rooms For Let makes it simple and effective to advertise your space to thousands of active room-seekers across the UK. Create your free listing today and connect with your next tenant or lodger quickly. Visit us at https://www.roomsforlet.co.uk to get started.